Atypical Hemolytic Uremic Syndrome Treatment Market: Growth Analysis & Forecast 2034

Get Your Sample Report Here: https://reedintelligence.com/market-analysis/atypical-hemolytic-uremic-syndrome-treatment-market/request-sample

Buy Now: https://reedintelligence.com/market-analysis/atypical-hemolytic-uremic-syndrome-treatment-market

Market Size

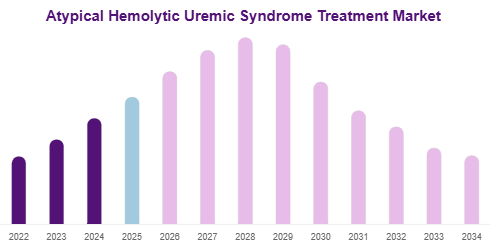

The global Atypical Hemolytic Uremic Syndrome Treatment Market size was valued at USD 3.12 billion in 2025.

It is projected to reach USD 6.85 billion by 2034, expanding at a CAGR of 9.1% during 2025–2034.

Introduction

The Atypical Hemolytic Uremic Syndrome Treatment Market is growing steadily due to increasing awareness of rare kidney disorders, improved diagnostic capabilities, and the availability of targeted therapies. Atypical hemolytic uremic syndrome (aHUS) is a rare and life-threatening disease characterized by abnormal blood clotting, kidney failure, and destruction of red blood cells.

The demand for effective treatment options is increasing as healthcare providers focus on early diagnosis and long-term disease management. Advances in complement inhibitor therapies are significantly transforming treatment outcomes.

Market Drivers

Rising Awareness of Rare Diseases

Healthcare organizations and patient advocacy groups are increasing awareness regarding rare disorders such as aHUS. Earlier diagnosis supports timely treatment initiation and improved survival rates.

Advancements in Targeted Therapies

The launch of complement inhibitor drugs has revolutionized treatment for aHUS patients. These therapies reduce disease recurrence, improve kidney function, and lower hospitalization rates.

Improved Healthcare Infrastructure

Developed nations with advanced healthcare systems are investing in rare disease treatment programs, reimbursement frameworks, and specialty care centers, driving market growth.

Market Challenges

High Treatment Costs

aHUS therapies, particularly biologics and complement inhibitors, are expensive. High annual treatment costs may limit access in low-income and middle-income countries.

Limited Patient Population

As a rare disease, the number of diagnosed patients remains relatively low, which can restrict revenue opportunities and clinical trial enrollment.

Diagnostic Complexity

Symptoms often overlap with other thrombotic microangiopathies, creating delays in accurate diagnosis and treatment.

Market Segmentation

By Treatment Type

Complement Inhibitors

Complement inhibitors held the dominant market share in 2025 due to strong clinical effectiveness and growing physician preference. These drugs remain the standard of care for many patients.

Plasma Therapy

Plasma exchange and plasma infusion continue to be used in selected cases, especially where biologic access is limited.

Supportive Care

Supportive care includes dialysis, blood pressure management, and transfusion therapy for acute disease management.

By Route of Administration

Intravenous

Intravenous therapies accounted for the largest share in 2025 as most approved biologic treatments are administered through infusion.

Subcutaneous

Subcutaneous treatments are expected to gain traction due to improved convenience and home-based administration potential.

By End User

Hospitals

Hospitals represented the leading segment owing to specialized nephrology and hematology treatment facilities.

Specialty Clinics

Specialty clinics are growing steadily due to personalized monitoring and chronic disease management services.

Research Institutes

Research centers contribute through clinical development and rare disease studies.

Regional Analysis

North America

North America dominated the market in 2025 due to high diagnosis rates, advanced treatment availability, and strong reimbursement support. The United States remains the major revenue contributor.

Europe

Europe held a significant share supported by rare disease policies, public healthcare coverage, and access to innovative biologics.

Asia Pacific

Asia Pacific is projected to witness the fastest CAGR through 2034 due to improving healthcare access, growing awareness, and expanding specialty care networks.

Latin America

Latin America is gradually expanding with better diagnostic infrastructure and improving treatment adoption.

Middle East & Africa

The region is witnessing moderate growth supported by specialty hospital investments and increasing rare disease recognition.

Top Players Analysis

The market is highly specialized, with leading companies focusing on biologics innovation, regulatory approvals, and geographic expansion.

- Alexion Pharmaceuticals, Inc. – Leading player with strong complement inhibitor portfolio for aHUS treatment.

- F. Hoffmann-La Roche Ltd. – Expanding rare disease pipeline and global healthcare reach.

- Novartis AG – Active in nephrology and specialty pharmaceutical innovation.

- Pfizer Inc. – Strong biologics and rare disease research capabilities.

- Amgen Inc. – Focused on advanced therapeutic development.

- Sanofi S.A. – Broad rare disease treatment presence worldwide.

- Takeda Pharmaceutical Company Limited – Strong specialty care portfolio.

- Regeneron Pharmaceuticals, Inc. – Innovative monoclonal antibody expertise.

- Biogen Inc. – Growing presence in rare disease therapeutics.

- AstraZeneca Plc – Expanding immunology and specialty medicine portfolio.