Orbital Atherectomy Market: Size, Growth Trends, Key Players & Forecast 2034

Market Size

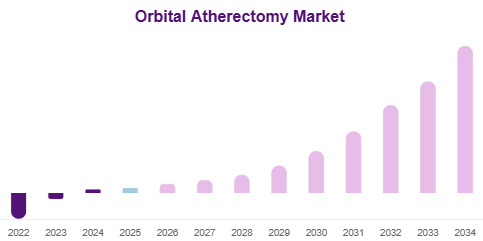

The global Orbital Atherectomy Market size was valued at USD 1.05 billion in 2026.

It is projected to reach USD 2.38 billion by 2034, expanding at a CAGR of 9.5% during 2026–2034.

Get Your Sample Report Here: https://reedintelligence.com/market-analysis/orbital-atherectomy-market/request-sample

Buy Now: https://reedintelligence.com/market-analysis/orbital-atherectomy-market

Introduction

The Orbital Atherectomy Market is witnessing strong growth due to the increasing burden of cardiovascular diseases worldwide and the rising preference for minimally invasive procedures. Orbital atherectomy systems are widely used to treat calcified coronary and peripheral artery lesions. These devices help improve vessel compliance, enable easier stent placement, and reduce recovery time for patients.

Healthcare providers are increasingly adopting these systems because they offer enhanced treatment precision, better procedural outcomes, and improved safety compared with conventional plaque-removal methods. As healthcare infrastructure expands globally, especially in emerging economies, the demand for orbital atherectomy solutions continues to rise.

Market Drivers

Rising Prevalence of Cardiovascular Diseases

The growing number of patients suffering from coronary artery disease and peripheral artery disease is one of the biggest growth factors for this market. Aging populations, sedentary lifestyles, diabetes, and obesity are increasing the incidence of arterial blockages, creating demand for advanced treatment devices.

Growing Demand for Minimally Invasive Procedures

Patients and healthcare providers prefer minimally invasive treatments because they reduce hospital stays, minimize complications, and offer faster recovery. Orbital atherectomy systems align with this trend, making them highly attractive in modern cardiovascular care.

Technological Advancements

Continuous innovation in crown coatings, orbital mechanisms, and device handling has significantly improved treatment efficiency. Modern systems provide better lesion modification with reduced risks, encouraging hospitals to invest in upgraded technologies.

Market Challenges

High Procedure and Device Costs

Orbital atherectomy systems are expensive, and procedures require trained specialists and advanced infrastructure. This limits adoption in developing nations where healthcare budgets remain constrained.

Reimbursement Limitations

In some countries, limited reimbursement policies for advanced cardiovascular interventions may restrict wider use of orbital atherectomy devices.

Availability of Alternative Treatments

Balloon angioplasty, stenting, and other atherectomy methods remain available alternatives, creating pricing and competitive pressure in the market.

Market Segmentation

By Application

Coronary Artery Disease

This segment dominated the market with a 58% share in 2024. The high prevalence of coronary artery disease and strong clinical effectiveness of orbital atherectomy in calcified coronary lesions support its leadership.

Peripheral Artery Disease

This segment is projected to grow at a CAGR of 10.4% through the forecast period due to rising awareness and increasing treatment of peripheral vascular disorders.

By Product Type

Orbital Atherectomy Systems

This segment held the largest market share of 68% in 2024. These systems are the primary treatment devices used in procedures and benefit from continuous design improvements.

Accessories & Consumables

This category is expected to grow steadily because each procedure requires recurring use of consumables and supporting accessories.

By End-Use

Hospitals

Hospitals accounted for 62% market share in 2024. Their dominance comes from advanced infrastructure, skilled specialists, and the ability to perform complex cardiovascular procedures.

Ambulatory Surgical Centers

This segment is forecast to grow at a CAGR of 10.8%, driven by cost-effective outpatient care and shorter patient recovery times.

Specialty Clinics

Specialty clinics are also expanding adoption due to focused cardiovascular care services and increased patient preference.

By End-User Specialty

Interventional Cardiology

This segment held the largest share of 55% in 2024 because cardiologists frequently use orbital atherectomy for coronary procedures.

Vascular Surgery

Growing use in peripheral artery treatments is expected to support future demand in vascular surgery settings.

Regional Analysis

North America

North America dominated the market with a 41% share in 2025. Strong healthcare infrastructure, reimbursement support, and rapid adoption of advanced devices drive regional leadership.

Europe

Europe held a 27% share in 2025, supported by rising awareness, medical innovation, and strong healthcare systems.

Asia Pacific

Asia Pacific accounted for 19% share in 2025 and is projected to grow at the fastest CAGR of 11.2%. Rising healthcare spending and medical tourism are key growth factors.

Top Players Analysis

- Cardiovascular Systems, Inc. – Market leader with strong product portfolio and continuous innovation.

- Medtronic plc – Global medical device giant with broad cardiovascular expertise.

- Boston Scientific Corporation – Strong presence in interventional cardiology solutions.

- Abbott Laboratories – Expanding cardiovascular device segment globally.

- Terumo Corporation – Strong distribution network and emerging market focus.

- Philips Healthcare – Advanced imaging integration capabilities.

- B. Braun Melsungen AG – Established medical technology provider.

- Cook Medical – Known for vascular intervention devices.

- MicroPort Scientific Corporation – Growing presence in Asia-Pacific markets.

- Biotronik SE & Co. KG – Focused on cardiovascular innovation.