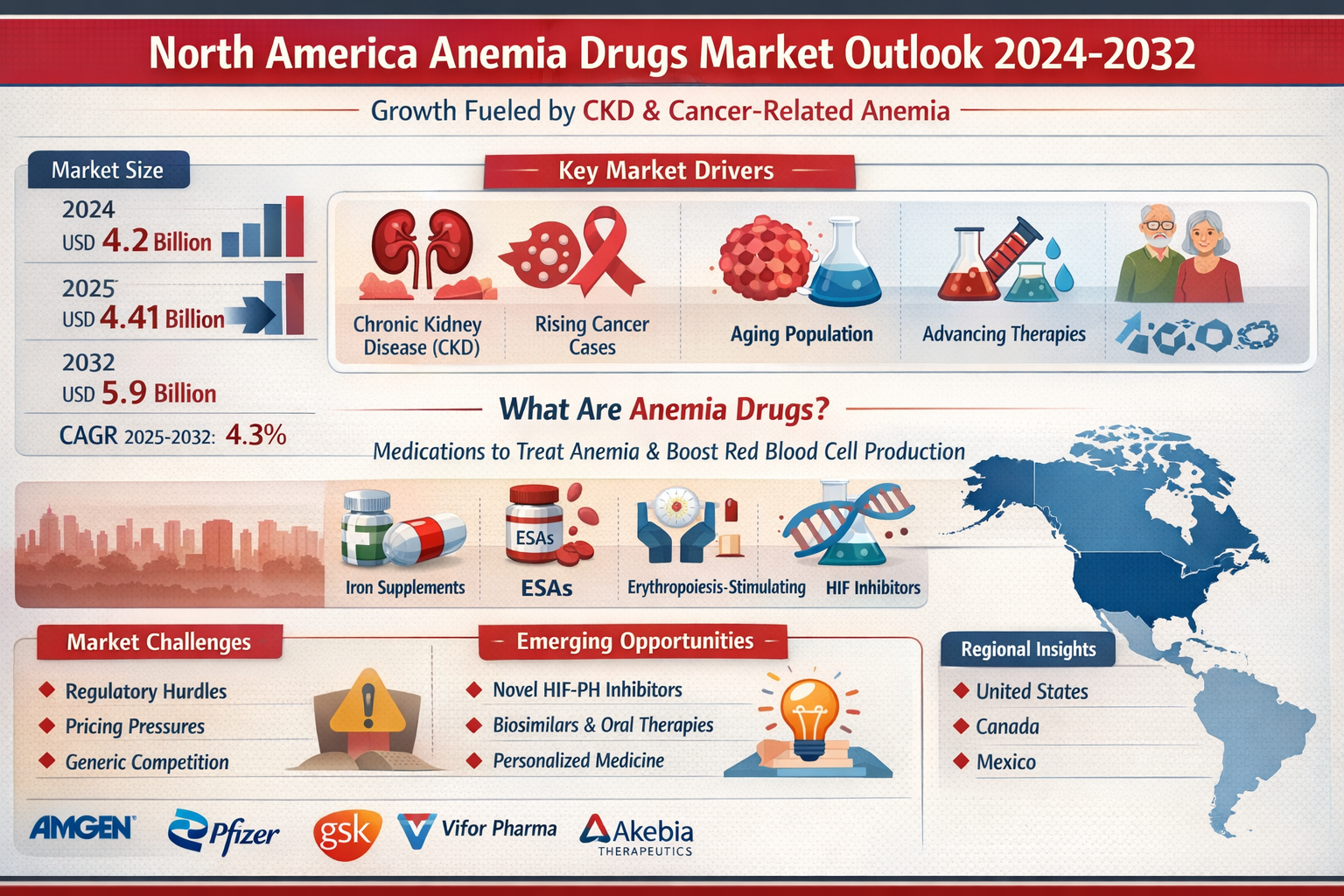

North America Anemia Drugs Market Set to Reach USD 5.9 Billion by 2032 Amid Rising CKD and Cancer Cases

According to a new report from Intel Market Research, the North America Anemia Drugs Market was valued at USD 4,200 million in 2024 and is projected to grow from USD 4,410 million in 2025 to reach USD 5,900 million by 2032, growing at a CAGR of approximately 4.3% during the forecast period (2025–2032). This steady expansion is driven by the high and growing prevalence of chronic kidney disease and cancer-related anemia in the aging North American population, well-established healthcare infrastructure, and continuous innovation in pharmaceutical therapeutics.

What Are Anemia Drugs?

Anemia drugs are pharmaceutical treatments designed to combat various types of anemia-a condition marked by a deficiency of red blood cells or hemoglobin in the blood, leading to reduced oxygen transport throughout the body. These drugs help increase red blood cell production, improve hemoglobin levels, and alleviate debilitating symptoms such as fatigue, weakness, and shortness of breath. The market encompasses a wide range of therapeutic agents including iron supplements, erythropoiesis-stimulating agents (ESAs), and novel therapies for anemia caused by chronic diseases like chronic kidney disease (CKD), cancer chemotherapy, and inflammatory conditions. The therapeutic landscape continues to evolve rapidly, with the emergence of hypoxia-inducible factor prolyl hydroxylase (HIF-PH) inhibitors representing a significant new class of orally administered treatments that offer a differentiated mechanism of action compared to conventional ESAs.

📥 Download FREE Sample Report:

North America Anemia Drugs Market - View in Detailed Research Report

This report provides a deep insight into the North America Anemia Drugs Market covering all its essential aspects-from a macro overview of the market to micro details such as market size, competitive landscape, development trends, niche markets, key drivers and challenges, SWOT analysis, and value chain analysis. The analysis helps the reader understand competition within the industry and strategies for enhancing profitability. Furthermore, it provides a framework for evaluating and accessing the position of a business organization. The report also focuses on the competitive landscape of the North America Anemia Drugs Market, introducing market share, performance, product positioning, and operational insights of major players. This helps industry professionals identify key competitors and understand the competition pattern.

In short, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those planning to foray into the North America Anemia Drugs Market.

Key Market Drivers

1. Prevalence of Chronic Kidney Disease (CKD) and Cancer

The primary engine for the North America Anemia Drugs Market is the high patient burden from underlying conditions that cause anemia. Chronic Kidney Disease (CKD) is a major contributor, with a significant portion of the regional patient population developing renal anemia as the disease progresses. The expanding cancer patient population undergoing chemotherapy-which frequently causes myelosuppressive anemia-similarly sustains strong, consistent demand for erythropoiesis-stimulating agents (ESAs) and iron therapies. The aging demographic profile of the United States and Canada further amplifies this demand, as both CKD and cancer incidence rise markedly with age, creating a structurally growing patient pool that requires long-term or episodic anemia management.

2. Advancements in Biologic and Biosimilar Therapies

Innovation in drug development continues to shape the market landscape. The introduction of longer-acting and novel mechanism ESAs has improved patient dosing convenience and outcomes. Concurrently, the emergence and growing acceptance of biosimilar ESAs are exerting competitive pricing pressure, enhancing patient access, and driving volume growth, particularly in cost-sensitive healthcare segments. Notably, in August 2023, GSK received U.S. FDA approval for its drug Jesduvroq (daprodustat) for anemia due to CKD in adults on dialysis-a milestone that highlights the continued pipeline innovation and regulatory momentum supporting market expansion. The strategic focus on patient-centric care and reducing transfusion dependency in chronic conditions is creating a stable, long-term demand pillar for pharmaceutical intervention.

3. Heightened Awareness and Improved Diagnostic Rates

Heightened clinical awareness and improved diagnostic protocols for anemia, especially in at-risk populations such as the elderly and individuals living with inflammatory diseases, are leading to earlier and more frequent treatment initiation. This trend is particularly pronounced in the United States, where robust physician education programs and expanding screening guidelines for chronic disease-related anemia are identifying patients who previously went undiagnosed and untreated, thereby expanding the effective treatment-eligible population across the region.

Market Challenges

- Stringent Regulatory Scrutiny and Safety Concerns – Legacy ESAs carry FDA-mandated boxed warnings regarding cardiovascular risks and potential tumor progression in certain cancers. This necessitates strict risk management programs (REMS) and influences prescribing patterns, often relegating these drugs to later-line therapy or specific risk-benefit profiles, thereby limiting their broader market potential.

- Pricing Pressures and Reimbursement Hurdles – Intense cost-containment efforts by payers, including the Centers for Medicare & Medicaid Services (CMS) in the U.S., lead to bundled payments and restrictive formularies. The influx of biosimilars, while increasing access, accelerates price erosion for branded biologics, squeezing manufacturer margins and complicating commercial strategy.

- Pipeline Attrition and High Development Costs – The development of novel anemia therapeutics, particularly for complex inflammatory anemias, is fraught with high costs and clinical trial risks. Late-stage failures of promising candidates have periodically disrupted the innovation pipeline, delaying new treatment options and forcing continued reliance on established drug classes with known limitations.

Market Restraints

Shift Towards Non-Pharmacological and Alternative Management

A key restraint for the North America Anemia Drugs Market is the growing clinical emphasis on managing the root cause of anemia rather than solely relying on drug therapy. For conditions like iron-deficiency anemia (IDA), first-line guidelines increasingly promote dietary modification and intravenous iron replenishment for severe cases, potentially reducing the long-term use of certain stimulating agents. In perioperative settings, enhanced blood conservation protocols are also minimizing routine prophylactic drug use, moderating demand in specific patient segments.

Patent Expiries and Generic Competition

The loss of patent exclusivity for key branded drugs, including oral iron formulations and earlier ESA brands, has opened the door to significant generic and biosimilar competition. This drastically reduces the revenue from these mature products and forces originator companies to defend market share through aggressive lifecycle management strategies or shift investment focus toward newer, patented innovations. This dynamic is fundamentally altering the competitive structure across the North America Anemia Drugs Market, compressing margins while simultaneously broadening patient access.

Emerging Opportunities

The North American healthcare landscape is increasingly favorable for innovative anemia drug development and commercialization. Several high-value opportunities are emerging that are expected to catalyze the next phase of market growth.

- Novel Therapies for Unmet Needs in Inflammation-Associated Anemia – The most significant opportunity lies in developing treatments for anemias where current ESAs are ineffective, such as anemia of inflammation (AI) and anemia of chronic disease (ACD). Targeted therapies addressing hepcidin pathways or hypoxia-inducible factor (HIF) physiology represent a frontier in the market, offering potential blockbuster revenues for first-to-market players addressing this large, underserved patient population.

- Expansion of Oral and Subcutaneous Formulations – There is a clear trend toward patient-friendly administration routes. The development of highly bioavailable oral iron therapies and convenient subcutaneous ESAs or HIF stabilizers enhances adherence, reduces the burden on infusion centers, and supports home-based care models-a shift that presents a substantial growth vector for companies that can effectively commercialize these alternatives.

- Personalized Medicine and Biomarker-Driven Treatment – Advancements in biomarker research enable more personalized treatment approaches. Identifying patient subgroups most likely to respond to specific therapies-based on ferritin levels, hepcidin concentrations, or genetic markers-can improve outcomes and justify premium pricing for targeted drugs, creating niche, high-value segments within the broader market.

📥 Download FREE Sample Report:

North America Anemia Drugs Market - View in Detailed Research Report

Market Segmentation

By Type

- Injection-based Therapies

- Oral Therapies

- Novel Biologics & Gene Therapies

By Application

- Chronic Kidney Disease (CKD) Anemia

- Iron Deficiency Anemia (IDA)

- Sickle Cell Disease & Hemolytic Anemias

- Cancer & Chemotherapy-Induced Anemia

- Others

By Drug Class

- Erythropoiesis-Stimulating Agents (ESAs)

- Iron Replacement Products

- Red Blood Cell Maturation Agents

- Novel Therapies & Biologics

By End User

- Hospitals & Inpatient Clinics

- Specialty & Outpatient Centers

- Retail Pharmacies & Home Care

By Distribution Channel

- Hospital Pharmacies

- Specialty Pharmacies

- Retail & Mail-Order Pharmacies

By Country

- United States

- Canada

- Mexico

📘 Get Full Report Here:

North America Anemia Drugs Market - View Detailed Research Report

Segment Analysis

Injection-based therapies represent the leading segment by type, driven by the dominant use of Erythropoiesis-Stimulating Agents (ESAs) and intravenous iron supplements for chronic and severe anemia cases. ESAs remain foundational for managing CKD-related anemia, a major indication within the region's well-structured nephrology care networks. The high efficacy and rapid hemoglobin correction offered by injectables align with clinical protocols in hospital and specialized care settings common in North America, and ongoing development of next-generation injectable biologics reinforces this segment's leadership despite the convenience factor of oral alternatives.

Among applications, Chronic Kidney Disease (CKD) Anemia holds the leading position as the most significant and well-defined therapeutic area. The high prevalence of CKD in the aging population creates a large, continuous, and clinically managed patient pool requiring long-term anemia management. Established reimbursement pathways and treatment guidelines specifically for CKD anemia within the U.S. and Canadian healthcare systems solidify this segment's dominance, while significant R&D investment and recent drug approvals continue to concentrate market focus and innovation here.

Erythropoiesis-Stimulating Agents (ESAs) represent the cornerstone therapeutic class by drug category, maintaining a central role in treatment protocols despite evolving competitive dynamics. Their long-standing position is anchored in decades of clinical use for oncology and nephrology, creating deeply ingrained physician familiarity and trust. While facing competition from novel agents and biosimilars, ESAs continue to serve as the first-line standard-of-care for raising hemoglobin levels in specific chronic anemia indications.

Hospitals and Inpatient Clinics constitute the primary end-user segment, serving as the central hub for diagnosis, complex case management, and administration of critical therapies. They are the first point of care for severe anemia cases, post-surgical anemia, and patients with comorbid conditions like advanced CKD or cancer requiring coordinated treatment. Hospital Pharmacies correspondingly dominate the distribution channel landscape, directly supplying high-volume, high-cost injectable biologics and intravenous iron required for inpatient and complex outpatient care.

Regional Market Insights

The United States stands as the undisputed leader within the North America Anemia Drugs Market, commanding the majority share due to its advanced healthcare infrastructure, high treatment adoption rates, and sophisticated patient care pathways. The market is heavily driven by a high prevalence of chronic kidney disease and cancer-related anemia, coupled with significant patient awareness and favorable reimbursement policies under both private and public insurance systems. Robust clinical research and significant investment in novel therapeutics-including next-generation ESAs, iron replacement therapies, and oral HIF-PH inhibitors-are concentrated in the U.S. Stringent yet clear regulatory oversight from the FDA ensures that drugs reaching the market meet high safety and efficacy standards, which in turn builds physician and patient confidence. The reimbursement environment through Medicare, Medicaid, and private insurers is a defining feature of the U.S. market, significantly influencing drug selection, pricing, and access.

Canada represents a significant and stable segment of the North America Anemia Drugs Market, characterized by a universal, publicly-funded healthcare system that ensures broad patient access to standard therapies. Market dynamics are strongly influenced by federal and provincial health technology assessment (HTA) bodies, such as CADTH and INESSS, which rigorously evaluate the clinical and cost-effectiveness of new drugs before formulary listing. While this creates a structured but sometimes more deliberate pathway for new anemia drug introductions compared to the U.S., the treatment landscape is well-established, with a high standard of care in nephrology and oncology driving steady demand for ESAs and iron products.

Mexico is an emerging and increasingly important growth market within the North America Anemia Drugs Market, driven by efforts to modernize its healthcare infrastructure and expand treatment access. The market is bifurcated between the private healthcare sector, which mirrors treatment patterns similar to the U.S., and the larger public sector, which focuses on cost-effective generics and essential medicines. Improving diagnosis rates for anemia, particularly in chronic disease populations, presents a significant opportunity for market expansion, attracting attention from both multinational and local drug manufacturers.

Evolving Market Trends

A primary trend shaping the North America Anemia Drugs Market is the strategic pivot towards innovative biologics and precision therapies for complex, chronic conditions. Pharmaceutical companies are heavily investing in R&D for novel ESAs with improved safety profiles and next-generation therapies like HIF-PH inhibitors, which offer a new oral mechanism of action. This focus is particularly pronounced in the United States, where advanced healthcare infrastructure and favorable reimbursement frameworks for specialty drugs support the adoption of high-value therapeutics-underscoring a market evolution from generic supplementation to targeted, condition-specific management.

A significant and transformative subtopic within the market is the burgeoning pipeline of gene and cell therapies, especially for rare anemias like sickle cell disease and beta-thalassemia. Following landmark regulatory approvals, several biopharmaceutical firms are advancing clinical trials for one-time curative treatments, supported by the FDA's fast-track designations and a robust venture capital ecosystem. While currently addressing niche patient populations, these therapies represent a paradigm shift in long-term disease management and are setting new standards for treatment outcomes. Market consolidation through mergers, acquisitions, and strategic collaborations is another defining trend, with leading players engaging in partnerships to broaden their portfolios, gain access to novel drug platforms, and mitigate the impact of patent expirations on blockbuster ESAs.

Competitive Landscape

The North America anemia drugs market is characterized by a moderately consolidated competitive structure dominated by a few multinational pharmaceutical giants with diversified portfolios and significant research and development capabilities. The commanding presence of companies like Amgen Inc., through its erythropoiesis-stimulating agents, and GlaxoSmithKline in the iron replacement and novel therapy segment, anchors the market. Leadership is maintained through continuous product innovation, lifecycle management of key brands, and strategic investments in clinical trials for next-generation biologics and targeted therapies. The competitive intensity is high, with players aggressively focusing on the lucrative chronic kidney disease and oncology-related anemia segments, where high treatment costs and specialized patient management create significant revenue opportunities.

Beyond the dominant leaders, a dynamic layer of specialized biotechnology and pharmaceutical companies compete in niche segments, driving innovation and market diversification. Entities such as Global Blood Therapeutics (now part of Pfizer), focused on sickle cell disease, and Akebia Therapeutics, developing novel treatments for anemia of CKD, exemplify this trend. The competitive landscape is further shaped by the entry of biosimilars, increasing generic competition for oral iron supplements, and a growing pipeline of gene and cell therapies targeting rare anemias.

List of Key Anemia Drugs Companies Profiled

- Amgen Inc.

- Pfizer Inc.

- Johnson & Johnson (Janssen Pharmaceuticals)

- GSK plc (GlaxoSmithKline)

- Vifor Pharma (part of CSL)

- Akebia Therapeutics, Inc.

- FibroGen, Inc.

- Bristol Myers Squibb (Celgene Corporation)

- Acceleron Pharma (a wholly-owned subsidiary of Merck & Co.)

- Bluebird Bio, Inc.

- Eli Lilly and Company

- Bayer AG

- Protagonist Therapeutics, Inc.

- Rockwell Medical, Inc.

- Mast Therapeutics (Activity status inactive; merger completed)

Report Deliverables

- North America market forecasts from 2025 to 2032, with country-level breakdowns for the U.S., Canada, and Mexico

- Strategic insights into pipeline developments, clinical trials, and regulatory approvals across key indications

- Market share analysis and SWOT assessments for major industry participants

- Pricing trends and reimbursement dynamics across public and private payer environments

- Comprehensive segmentation by drug type, therapeutic application, drug class, end user, and distribution channel

📘 Get Full Report Here:

North America Anemia Drugs Market - View Detailed Research Report

📥 Download FREE Sample Report:

North America Anemia Drugs Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

- Real-time competitive benchmarking

- Global clinical trial pipeline monitoring

- Country-specific regulatory and pricing analysis

- Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us