Stainless Steel Turning Inserts Market Size, Share & Forecast 2026–2036

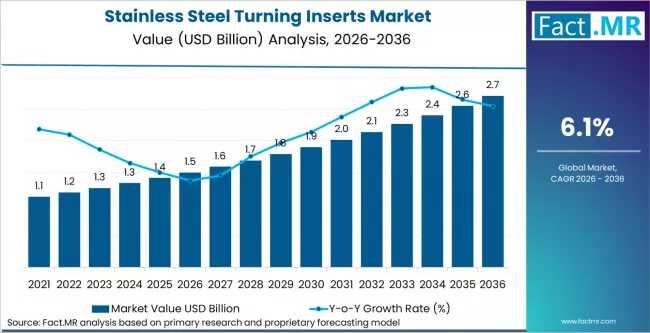

The global industrial landscape is undergoing a rigorous transition toward high-precision, difficult-to-machine alloys, placing the Stainless Steel Turning Inserts Market at the center of a significant valuation surge. According to the latest strategic analysis by Fact.MR, the market is positioned to grow from USD 1.5 billion in 2026 to a commanding USD 2.7 billion by 2036.

This projected expansion represents a near-doubling of market value within the decade. As manufacturers in the automotive, aerospace, and medical device sectors grapple with the complexities of austenitic and duplex stainless steels, the demand for specialized carbide substrates and advanced coating architectures has reached a critical inflection point.

Get Access Sample Report: https://www.factmr.com/connectus/sample?flag=S&rep_id=14598

Efficiency Gains Drive the USD 1.2 Billion Opportunity

The primary catalyst for this growth is the relentless pursuit of ""cost-per-part"" optimization. In high-volume environments like automotive manufacturing—which is projected to command a 53% market share by 2026—the ability to maintain edge consistency at elevated cutting speeds is no longer a luxury but a structural necessity.

The market is currently underpinned by a massive tooling upgrade cycle,"" says Shambhu Nath Jha, Principal Consultant at Fact.MR. ""Decision-makers are moving away from general-purpose grades in favor of application-specific geometries. We are seeing a distinct shift where Chemical Vapor Deposition (CVD) coatings are achieving a dominant 40% share because they offer the thermal stability required for the next generation of stainless alloy components.""

Key Market Dynamics and Strategic Trends

Thermal Resistance via CVD Dominance: CVD-coated inserts are outpacing traditional PVD options in high-speed applications. Innovations from leaders like Sandvik Coromant (GC4415/GC4425 series) have demonstrated tool life increases of up to 25%, directly impacting the bottom line for Tier 1 suppliers.

Aerospace & Medical Precision: Beyond automotive, the aerospace sector’s reliance on super-austenitic grades for turbine parts and the medical industry’s demand for ISO 9001-compliant surgical instruments are creating a ""recess-proof"" recurring demand for premium inserts.

Raw Material Volatility: While growth is robust, the industry faces structural constraints from cobalt and carbide substrate price fluctuations, forcing manufacturers to innovate with multi-edge geometries that maximize material utility.

Regional Growth Engines: The Rise of Asia and Germany

The geography of the market is shifting toward regions with aggressive industrial modernization programs:

China (8.8% CAGR): Leads global growth, fueled by the 14th Five-Year Plan and massive expansions in EV battery enclosure production by giants like BYD.

India (7.9% CAGR): Benefiting from the Production Linked Incentive (PLI) scheme, India is rapidly becoming a global hub for stainless steel component exports.

Germany (7.3% CAGR): Remains the high-value benchmark, with BMW Group and Mercedes-Benz pushing the limits of high-precision stainless alloy turning.

United States (6.0% CAGR): Driven by long-term defense contracts with Boeing and Raytheon Technologies, focusing on high-performance aerospace alloys.

Competitive Landscape: Performance as a Moat

The market is characterized by a ""performance-first"" competitive strategy. While regional players in Asia compete on price in the mid-range segment, global leaders are securing long-term contracts through digital tooling management and ""tooling-as-a-service"" platforms.

Key Industry Participants Include: Sandvik Coromant, KYOCERA, Kennametal, Mitsubishi Materials Corporation, Sumitomo Corporation, Seco Tools, Walter Tools, Dormer Pramet, Korloy, and ISCAR.

Strategic Outlook

For investors and CXOs, the roadmap is clear: the integration of advanced coating technology with specific alloy families (such as duplex stainless steel for oil and gas) represents the highest-margin frontier. As the market adds USD 1.2 billion in value over the next ten years, the advantage will belong to those who prioritize application engineering over commodity supply.

About Fact.MR Fact.MR is a distinguished market research agency and growth consultancy. We provide comprehensive insights into highly specialized industry verticals, empowering decision-makers with the data necessary to navigate complex global supply chains. Our methodology combines deep primary research with advanced econometric modeling to deliver actionable intelligence.

To View Related Report :

Stainless Steel Panels Market https://www.factmr.com/report/stainless-steel-panels-market

Steel Surface Conditioning And Descaling Systems Market https://www.factmr.com/report/steel-surface-conditioning-and-descaling-systems-market

Steel Plant Fire Protection Systems Market https://www.factmr.com/report/steel-plant-fire-protection-systems-market

Steel Coil Handling Equipment Market https://www.factmr.com/report/steel-coil-handling-equipment-market

United Kingdom Steel Pipe Coatings Industry Analysis https://www.factmr.com/report/united-kingdom-steel-pipe-coatings-industry-analysis

Steel Tubes Market https://www.factmr.com/report/480/steel-tubes-market

Steel Casing Pipes Market https://www.factmr.com/report/5140/steel-casing-pipes-market

Green Steel Market https://www.factmr.com/report/green-steel-market