Snacks Market to Expand by USD 385.54 Billion by 2036 at 5.1% CAGR

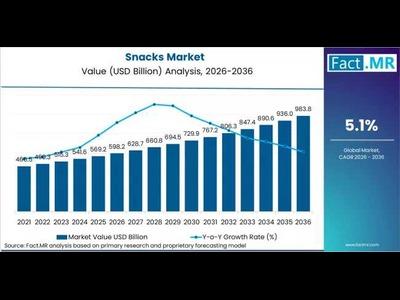

The global snacks market is undergoing a profound structural evolution, projected to grow from USD 598.23 billion in 2026 to a commanding USD 983.77 billion by 2036. According to the latest strategic forecast by FACT.MR, the industry will expand at a 5.1% CAGR, adding USD 385.54 billion in absolute dollar growth as snacks increasingly replace full meals and "better-for-you" reformulations take center stage.

As global supply chains mature, the market is moving beyond simple price competition. Future growth is now anchored in regulatory compliance, sustainability performance, and the premiumization of salty snacks. Analysts identify India and the USA as the primary engines of this expansion, fueled by infrastructure investment and a shift toward organized retail.

Get Access Report Sample : https://www.factmr.com/connectus/sample?flag=S&rep_id=50

Quick Stats: Snacks Market at a Glance

- Market Value (2026E): USD 598.23 Billion

- Projected Value (2036F): USD 983.77 Billion

- Forecast CAGR:1% (2026–2036)

- Leading Product Segment: Salty Snacks (35.0% share)

- Dominant Source Ingredient: Maize & Wheat (35.0% share)

- Top Growth Market: India (5.4% CAGR)

Product & Ingredient Insights: The Power of Salty and Staple Bases

The snack landscape remains dominated by savory flavors and versatile, low-cost ingredients that allow for mass-market scalability.

Salty Snacks (35.0% share):

Potato chips, tortilla chips, and pretzels remain the core of the category. This segment benefits from the highest repurchase frequency in the industry, driven by flavor innovation. Major players like PepsiCo are accelerating this trend, having launched dozens of new flavor variants globally in recent months to maintain high consumer engagement.

Maize & Wheat (35.0% share):

As a source ingredient, corn and wheat provide the lowest-cost base with maximum processing versatility. While corn extrusion dominates in volume, wheat-based snacks are being repositioned toward whole-grain formulations to meet evolving nutritional targets like the US FDA’s health claim frameworks and Europe’s "Farm to Fork" strategy.

Strategic Distribution:

Hypermarkets and convenience stores continue to lead, but organized retail expansion into Tier 2 and Tier 3 cities—particularly in India—is fundamentally lowering risk-adjusted entry costs for global brands.

Regional Performance: Divergent Growth Trajectories

While the global average sits at 5.1%, key nations are outperforming the baseline through aggressive retail formalization and health-centric labeling policies.

|

Country |

Projected CAGR |

Primary Growth Catalyst |

|

India |

5.4% |

Organized retail expansion in Tier 2/3 cities and rising disposable income. |

|

USA |

5.0% |

Premiumization of salty snacks and meal-replacement functional products. |

|

Germany |

4.7% |

Reformulation under Nutri-Score labeling and organic category growth. |

Structural Drivers & Structural Shifts

Key Market Drivers:

- Formalization of Retail: Organized trade in emerging markets is reducing per-unit logistics costs and expanding the accessible buyer base.

- The "Meal Replacement" Trend: Particularly in the U.S., snacks are replacing full meals, driving demand for protein-rich and functional ingredients.

- Regulatory Momentum: Mandatory technical standards and labeling (like HFSS restrictions in the UK and Nutri-Score in Germany) are forcing rapid product upgrades.

Strategic Restraints:

- Compliance Complexity: Suppliers operating in five or more national markets face significant certification burdens that require dedicated regulatory infrastructure to manage.

Competitive Landscape: Compliance is the New Competition

The snacks market is entering a consolidation phase. Leading participants, including PepsiCo Inc., Nestlé S.A., Mondelez International, and ITC Limited, are being selected by institutional buyers based on their certification records and sustainability performance rather than price alone. Vendors unable to document environmental accountability across their full production chain face exclusion from top-tier procurement cycles.

Analyst Opinion:

"We are seeing a clear transition where technology differentiation and regulatory compliance capacity are replacing price as the primary vendor selection criteria. In the next decade, the 'winners' will be those who can navigate the complex web of global food safety and sustainability standards while maintaining a rapid cadence of flavor innovation." — Senior Market Analyst, FACT.MR

Interactive Next Step

Would you like me to prepare a Regional Attractiveness Scorecard comparing the investment-readiness of Southeast Asia vs. Latin America based on current organized retail penetration and logistics infrastructure?

To View Related Report:

Fruit Snacks Market https://www.factmr.com/report/4476/fruit-snacks-market

Jerky Snacks Market https://www.factmr.com/report/jerky-snacks-market

No Fat Snacks Market https://www.factmr.com/report/no-fat-snacks-market

Healthy Snacks Market https://www.factmr.com/report/healthy-snacks-market