Animal Gastroesophageal Reflux Disease Industry to Expand by USD 1.5 Billion by 2035

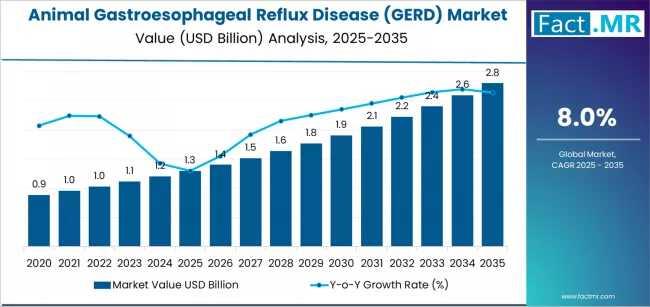

The global animal gastroesophageal reflux disease (GERD) market is entering a period of robust structural expansion, projected to grow from USD 1.3 billion in 2025 to USD 2.8 billion by 2035. According to a definitive market outlook by Fact.MR, the sector is expanding at a 8.0% CAGR, catalyzed by the rising "humanization" of pets, increasing veterinary specialty clinic networks, and a global surge in companion animal ownership.

As pet owners increasingly prioritize evidence-based medical interventions, the market is shifting from basic symptomatic relief toward advanced, species-specific pharmaceuticals. Proton Pump Inhibitors (PPIs) have emerged as the dominant therapeutic class, capturing 41.0% of the market, praised by veterinarians for providing symptom resolution rates of 75-85% in feline and canine patients.

Get Access Report Sample :

https://www.factmr.com/connectus/sample?flag=S&rep_id=11727

Quick Stats: Animal GERD Market at a Glance

- Market Value (2025E): USD 1.3 Billion

- Projected Value (2035F): USD 2.8 Billion

- Forecast CAGR:0% (2025–2035)

- Leading Drug Segment: Proton Pump Inhibitors (41.0% share)

- Dominant Animal Type: Companion Animals (63.0% share)

- Growth Hotspot: India (8.9% CAGR)

Therapeutic Dynamics: The Dominance of PPIs

The market’s expansion is heavily influenced by the efficacy of modern acid-suppression mechanisms.

Proton Pump Inhibitors (41.0% share):

PPIs, particularly omeprazole-based formulations (which hold 58.0% of this segment), are the gold standard for treating severe esophageal inflammation. Their once-daily dosing and high safety margins make them the preferred choice for chronic disease management in veterinary hospitals.

H2 Receptor Blockers (28.0% share):

These remain vital for mild-to-moderate cases and acute symptom control, offering a shorter duration of action that appeals to owners managing intermittent reflux issues.

Supportive Therapies:

Antacids (19.0%) and Prokinetic agents (12.0%) continue to play a critical role in adjunctive therapy, specifically in cases requiring improved gastric motility and esophageal sphincter function.

Distribution Channels: The Rise of Specialized Veterinary Care

Veterinary Hospitals & Clinics (55.0% share):

Professional facilities remain the primary gateway for GERD diagnosis and treatment. Specialty and referral hospitals, which account for 42.0% of this segment, are driving the adoption of complex treatment protocols and endoscopic evaluation.

Online & Retail Pharmacies (45.0% combined share):

E-commerce and pet-specific retail pharmacies are growing rapidly. The rise of telemedicine-integrated prescription fulfillment (15.0% of the total market) is making it easier for pet owners to maintain long-term treatment regimens without frequent clinic visits.

Regional Performance: Asia-Pacific Outpacing Global Averages

While the United States (8.3% CAGR) remains the value leader due to high pet insurance penetration (68% in urban markets), India is the world's fastest-growing corridor.

|

Country |

Projected CAGR |

Primary Growth Catalyst |

|

India |

8.9% |

Rapid adoption of companion animals among the urban middle class. |

|

USA |

8.3% |

Established specialty care infrastructure and high diagnostic awareness. |

|

China |

8.1% |

Accelerated urbanization and pet humanization trends. |

|

Germany |

7.7% |

Strong owner investment in premium veterinary services and high compliance. |

|

Japan |

7.5% |

An aging pet population requiring advanced gastrointestinal monitoring. |

Strategic Drivers & Industry Challenges

Market Drivers:

- Pet Humanization: Owners are increasingly seeking medical care for pets that mirrors human standards.

- Diagnostic Advancement: Wider availability of veterinary endoscopy and specialized pH monitoring.

- Insurance Integration: Growth in pet insurance coverage is making expensive, long-term pharmaceutical treatments more accessible.

Market Restraints:

- High Formulation Costs: The technical requirement to optimize drug palatability for different species increases manufacturing expenses.

- Regulatory Complexity: Stringent validation standards for animal-specific drug approvals can delay market entry for new formulations.

- Supply Chain Volatility: Fluctuating costs of active pharmaceutical ingredients (APIs) for veterinary-grade medications.

Competitive Landscape

The market features a concentrated group of animal health giants, including Zoetis Inc., Boehringer Ingelheim, Elanco, and Virbac. Competitive differentiation is increasingly found in palatability-enhanced formulations and integrated diagnostic-therapeutic platforms that help veterinarians monitor clinical outcomes in real-time.

To View Related Report:

Animal Antibiotics and Antimicrobials Market https://www.factmr.com/report/animal-antibiotics-and-antimicrobials-market

Animal Osteoarthritis Market https://www.factmr.com/report/animal-osteoarthritis-market

Animal Intestinal Health Market https://www.factmr.com/report/animal-intestinal-health-market

Animal Drug Compounding Market https://www.factmr.com/report/animal-drug-compounding-market

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.